Tax Liens & Tax Deeds:

A Secure, High-Yield Investment, or Is It?

Tax Liens and Tax Deeds as an Investment Opportunity at 4 Square Investments

Tax Liens and Tax Deeds as an Investment Opportunity at 4 Square Investments

Tax liens and tax deeds are tools local governments use to recover unpaid property taxes. When owners become delinquent, counties or municipalities may sell either a tax lien (a claim against the property) or a tax deed (rights to the property itself) to investors. This creates opportunities to earn interest or penalties on the unpaid taxes, or—in fewer cases—acquire the underlying real estate.

At 4 Square Investments, the focus is on providing clear educational information so investors can make informed decisions. Our team performs sourcing and due diligence on opportunities presented. Deals are SEC-compliant and available to accredited and non-accredited investors, with some IRA-eligible options. The firm has facilitated nearly $200mm across hundreds of thousands of lien and deed acquisitions with a team possessing 50+ years of combined real estate experience.

Understanding Tax Liens and Tax Deeds

Tax Liens (Tax Certificates): The investor pays the delinquent taxes to the government and receives a senior lien on the property along with the right to collect statutory interest or penalties. The original owner has a redemption period to repay the full amount (taxes plus the investor’s return). If the owner does not redeem, the investor may begin foreclosure proceedings, which can lead to a tax deed sale or transfer of ownership under state-specific rules.

Tax Deeds: The government auctions the property deed (or a redeemable interest in it) directly to recover the unpaid taxes. The buyer may gain ownership rights, often subject to a redemption period in which the original owner can reclaim the property by paying the sale price plus required penalties or costs.

Tax liens and deeds generally hold priority over many other claims on the property (such as junior mortgages in many jurisdictions), but exact priority rules, bidding methods, and procedures differ significantly by state and even by county. Redemption rates are typically high—often 90–98% or more nationally—meaning most investments result in interest or penalty income rather than property ownership.

Before the Sale (Pre-Registration and Preparation): Many jurisdictions require pre-registration days or weeks in advance. This often involves submitting forms such as a W-9 (for tax reporting), a registration declaration, proof of identity, and sometimes a deposit or proof of funds. Online auction platforms (common in states like Florida, Illinois, or Colorado) may require creating an account, providing banking information for electronic payments, and receiving county approval. In some counties, registration deadlines are strict with no late entries allowed. Investors should review the specific county’s auction notice or website for required documents, deadlines, and any bidder qualifications (e.g., restrictions on certain entities or individuals).

At the Sale (During the Auction): On auction day (or for online sales, during the active bidding window), registered bidders typically receive a bidder number. Payment rules are strict—most counties require immediate or same-day payment in cash, cashier’s check, certified funds, or wire/electronic transfer. Personal checks are usually not accepted. Some auctions allow bidding in person at the courthouse, while others are fully online. Bidders must often bring government-issued ID and tax identification information. In certain cases, a deposit may be required to participate, and winning bidders must complete payment within a short window (e.g., immediately or within one hour). Proxy bidding or representatives may be permitted in some locations if proper authorization and funds are arranged in advance.

These requirements help ensure orderly auctions and financial accountability. Investors new to the process should carefully read each county’s bidder instructions, as non-compliance can result in disqualification.

State Variations in Legal Processes and Opportunities

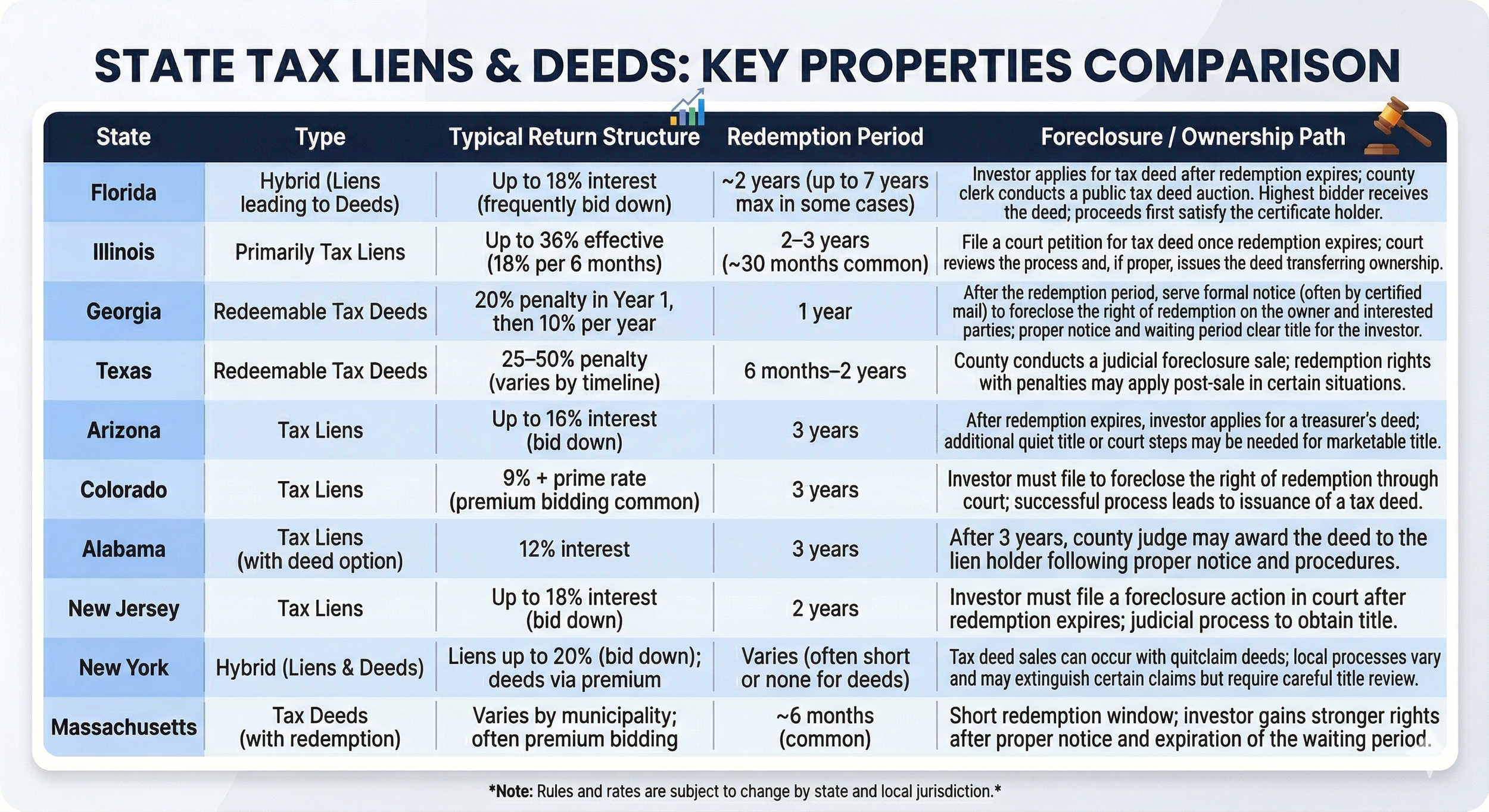

State laws create substantial differences in investment type, potential returns, redemption periods, bidding formats (e.g., interest rate bid-down vs. premium over taxes), and the steps required for foreclosure or ownership transfer. Below is an expanded summary for selected states:

State laws determine returns, timelines, redemption rights, and the path to ownership. Below is a summary for selected states:

Redemption rates are typically high (often 90–98% in many areas), meaning most investments result in interest or penalty income rather than property transfer. Foreclosure, when it occurs, involves additional steps such as applications, notices, court filings, or public auctions, with associated costs and timelines that differ by state.

Legal and Educational Notes on State Variations

Beyond the summary in the table, several important legal principles apply across jurisdictions and deserve careful attention:

Bidding Mechanisms: States use different auction formats. In “bid-down” states (such as Florida, Illinois, and New Jersey), investors compete by offering lower interest rates than the statutory maximum. In “premium bid” states (common in Colorado or certain Massachusetts municipalities), investors compete by paying more than the tax amount, which can reduce or eliminate the effective return but may accelerate ownership rights.

Lien Priority and Super-Priority: Tax liens generally enjoy “super-priority” status, meaning they can take precedence over most existing mortgages or private liens. However, certain federal claims (such as IRS tax liens in limited circumstances) or specific governmental liens may retain priority or require separate handling.

Bankruptcy Implications: If the property owner files for bankruptcy during the redemption or foreclosure period, an automatic stay under federal bankruptcy law can pause all collection and foreclosure actions. This may extend timelines significantly and require the investor (or their representative) to seek relief from the bankruptcy court.

Title and Quiet Title Actions: Even after receiving a tax deed, the investor may not automatically hold fully marketable title. Additional legal steps—such as a quiet title lawsuit—are often necessary to clear any remaining clouds on title, unrecorded interests, or procedural defects from the original sale.

County-Level Variations: Within the same state, individual counties may have different administrative practices, notice requirements, or even slightly different interpretations of state statutes. This makes county-specific research and compliance essential.

These legal details illustrate why tax lien and tax deed investing is jurisdiction-specific and why professional due diligence and ongoing monitoring are importan

The Foreclosure Process: Educational Overview

When a property is not redeemed, the path to ownership (or resolution) is called the foreclosure process in tax lien contexts or the post-sale clearance in tax deed contexts. This is not a uniform national procedure—it is governed entirely by state and local law and often involves multiple steps:

Expiration of Redemption Period: The owner’s legal right to repay ends. In lien states, this triggers the investor’s right to act.

Notice Requirements: Many states require formal notice (certified mail, publication in newspapers, or posting on the property) to the original owner, occupants, and any recorded interest holders (e.g., mortgagees). Failure to provide proper notice can invalidate later steps.

Application or Filing: In tax lien states like Florida or Illinois, the investor typically files an application or court petition for a tax deed. In hybrid or deed states, the process may involve requesting a treasurer’s deed or confirming the sale.

Court or Administrative Review: Judicial states (e.g., Illinois, New Jersey, Colorado) require court approval. Non-judicial or administrative processes (common in some deed states) may be faster but still demand compliance with strict timelines and documentation.

Public Auction or Deed Issuance: In many cases (especially Florida), unredeemed properties go to a public tax deed auction where the highest bidder wins ownership. Proceeds first repay the original certificate holder plus costs; any surplus may return to the former owner.

Quiet Title or Additional Steps: Even after receiving a deed, investors often need to clear any remaining clouds on title through quiet title actions, especially if other liens or claims exist.

Key Educational Point: The entire foreclosure process can add months or years and involve legal fees, court costs, and administrative expenses. Because redemption rates are high, most investors never reach this stage. When they do, the goal is often to recover the invested amount plus return rather than necessarily taking ownership.

Common Myths About Tax Lien and Tax Deed Investing

Myth: Investors routinely receive the maximum statutory interest rate (e.g., 18% or 36%). Reality: Competitive auctions frequently reduce yields through bid-down mechanisms or premium bidding.

Myth: Most investments result in acquiring property at a deep discount. Reality: High redemption rates (often 90–98% nationally) mean the majority resolve as interest or penalty income. Property acquisition via foreclosure is the exception.

Myth: This is a completely passive investment requiring no ongoing effort. Reality: Monitoring, paperwork, sending notices, or pursuing foreclosure steps may be necessary, even with professional management.

Myth: You can easily buy properties for pennies on the dollar with clean title. Reality: Competition for desirable properties is strong, and issues such as additional liens, property condition, environmental concerns, or title complications frequently arise.

Myth: Tax sales always eliminate all prior liens, including mortgages. Reality: Priority rules vary by state; in some jurisdictions certain senior or specific liens (e.g., IRS in limited cases) may survive or require separate handling.

Myth: The process is simple and uniform across the country. Reality: Significant differences in bidding, redemption rights, notice requirements, judicial vs. non-judicial processes, and timelines make careful, state-specific due diligence essential.

Considerations for Investors

Curated opportunities typically target returns in the 8–18%+ range, though actual results depend on the specific deal, state laws, auction outcomes, and redemption behavior. Resolution timelines commonly range from 6 to 36 months, but foreclosure can extend this significantly.

These investments offer real estate collateral exposure and portfolio diversification, but they carry specific risks:

High redemption rates limit property acquisition opportunities.

Competitive bidding can lower effective yields.

Due diligence is critical regarding property condition, title status, additional encumbrances, and environmental factors.

Foreclosure involves variable legal costs, strict procedural compliance, and timelines that differ by jurisdiction.

Liquidity is generally limited until redemption or final resolution occurs.

Our team reviews opportunities before presentation, but every investor should perform independent analysis and consult qualified professionals.

Additional Information

Tax lien and tax deed investing requires thorough understanding of jurisdiction-specific legal and procedural details. Outcomes are not guaranteed, and past performance does not indicate future results. Key additional considerations include the need for detailed due diligence on each property (condition, market value, occupancy, zoning, and potential environmental or access issues), as the underlying asset ultimately backs the investment. Investors should also account for possible ongoing costs, such as paying subsequent taxes or liens to protect their position, and recognize that auctions have become more competitive with greater institutional participation in recent years.

Legislative and court changes can occur, affecting rules in specific states (for example, shifts in bidding structures or surplus equity handling). Bankruptcy filings by property owners can introduce delays via automatic stays. Even after acquiring a deed, achieving fully marketable title often requires extra steps and costs. Because of these factors, many participants treat this as a longer-term strategy focused primarily on interest or penalty income rather than routine property ownership.

4 Square Investments

All investments involve risk, including the potential loss of principal. Tax lien and tax deed investing carries jurisdiction-specific legal, title, market, and procedural risks. Rules and processes can change. Please consult your financial advisor, tax professional, and legal counsel before making any investment decisions.